Page 87 - 한국감정평가사협회 추천제도 설명자료_단면

P. 87

한국감정평가사협회 추천제도 설명자료

■ 감정평가 독립성 확보는 한국만의 특수한 조건이 아니다. 감정평가산업이 발달한 미국의 경우

에도 법률에 감정평가사의 독립성 보장을 명확히 규정하고 있다.

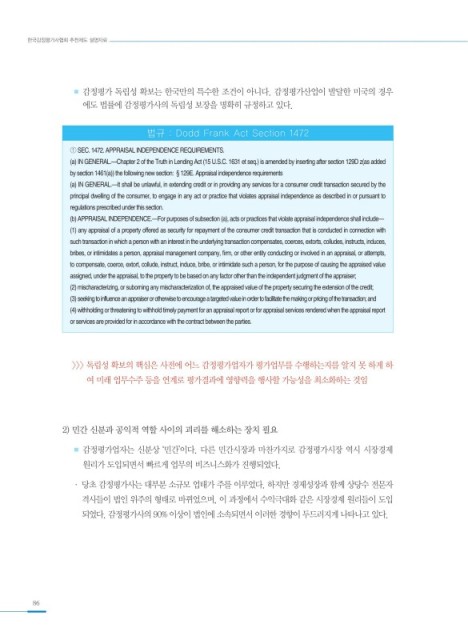

법규 : Dodd Frank Act Section 1472

① SEC. 1472. APPRAISAL INDEPENDENCE REQUIREMENTS.

(a) IN GENERAL.—Chapter 2 of the Truth in Lending Act (15 U.S.C. 1631 et seq.) is amended by inserting after section 129D z(as added

by section 1461(a)) the following new section: § 129E. Appraisal independence requirements

(a) IN GENERAL.—It shall be unlawful, in extending credit or in providing any services for a consumer credit transaction secured by the

principal dwelling of the consumer, to engage in any act or practice that violates appraisal independence as described in or pursuant to

regulations prescribed under this section.

(b) APPRAISAL INDEPENDENCE.—For purposes of subsection (a), acts or practices that violate appraisal independence shall include—

(1) any appraisal of a property offered as security for repayment of the consumer credit transaction that is conducted in connection with

such transaction in which a person with an interest in the underlying transaction compensates, coerces, extorts, colludes, instructs, induces,

bribes, or intimidates a person, appraisal management company, firm, or other entity conducting or involved in an appraisal, or attempts,

to compensate, coerce, extort, collude, instruct, induce, bribe, or intimidate such a person, for the purpose of causing the appraised value

assigned, under the appraisal, to the property to be based on any factor other than the independent judgment of the appraiser;

(2) mischaracterizing, or suborning any mischaracterization of, the appraised value of the property securing the extension of the credit;

(3) seeking to influence an appraiser or otherwise to encourage a targeted value in order to facilitate the making or pricing of the transaction; and

(4) withholding or threatening to withhold timely payment for an appraisal report or for appraisal services rendered when the appraisal report

or services are provided for in accordance with the contract between the parties.

>>> 독립성 확보의 핵심은 사전에 어느 감정평가업자가 평가업무를 수행하는지를 알지 못 하게 하

여 미래 업무수주 등을 연계로 평가결과에 영향력을 행사할 가능성을 최소화하는 것임

2) 민간 신분과 공익적 역할 사이의 괴리를 해소하는 장치 필요

■ 감정평가업자는 신분상 ‘민간’이다. 다른 민간시장과 마찬가지로 감정평가시장 역시 시장경제

원리가 도입되면서 빠르게 업무의 비즈니스화가 진행되었다.

· 당초 감정평가사는 대부분 소규모 업태가 주를 이루었다. 하지만 경제성장과 함께 상당수 전문자

격사들이 법인 위주의 형태로 바뀌었으며, 이 과정에서 수익극대화 같은 시장경제 원리들이 도입

되었다. 감정평가사의 90% 이상이 법인에 소속되면서 이러한 경향이 두드러지게 나타나고 있다.

86